When a property owner passes away, the family is often thrust into a whirlwind of legal and financial mandates. Amidst the grief, a crucial window of opportunity opens regarding the family’s largest asset: the real estate. This is where the “Date of Death” (DOD) appraisal—often called a retrospective appraisal—becomes your most powerful defensive tool.

The Power of the “Step-Up in Basis” Most homeowners understand that if they sell a house for more than they bought it for, they may owe capital gains tax. However, the IRS provides a significant “reset” button for heirs known as a Step-up in Basis.

Imagine a property in the El Dorado foothills purchased decades ago for $150,000 that is now worth $950,000. If the heirs sell it, they could be looking at a tax bill on $800,000 of gain. However, by obtaining a professional appraisal tied specifically to the owner’s date of passing, the “basis” jumps from the original $150,000 to the current market value.

Why timing is everything: If the market continues to climb after your loved one passes, your tax liability—for the purpose of the estate—is effectively “frozen” at that DOD value. Without a professional appraisal to document that specific moment in time, you are left guessing, and the IRS is rarely fond of guesswork.

How We Step Back in Time You might wonder: “How can you value my house as it was six months or two years ago?” As an appraiser, I perform a forensic analysis of the market. I don’t just look at what is happening today; I look at the specific inventory, interest rates, and buyer demand that existed on that exact calendar date. Whether the property is a suburban home in Roseville or a sprawling acreage in Amador, I reconstruct the narrative of that day’s market to ensure your CPA has a defensible, bulletproof document for tax filings.

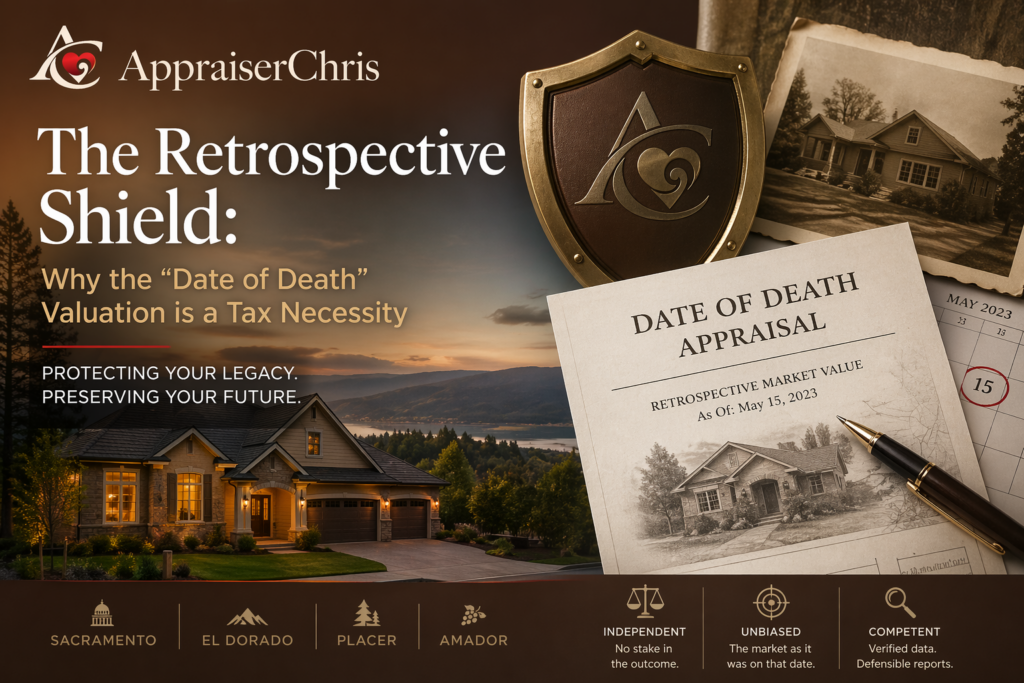

The Appraiser’s Promise – In these sensitive transitions,

- I do not advocate for a person, a price, or a deal. Under USPAP (Uniform Standards of Professional Appraisal Practice),

- I am required to be: Independent: I have no stake in the estate’s outcome or the eventual sale price.

- Unbiased: I interpret the market as it truly was on that date, without influence from heirs or external pressures.

- Competent: I utilize verified, historical data across our four-county region to support a narrative that stands up to scrutiny.

[email protected] | www.AppraiserChris.com | Serving Sacramento, El Dorado, Placer, and Amador Counties, Northern California